Post-COVID-19: Re-sets in the Way Ahead

My dissertation at Columbia University was entitled: “On Historical Change: Order Within Chaos.” And one of the key thrusts of my analysis was that crises are necessary forcing function events which allow for key emergent trends evident BEFORE the crisis to become the dominant forces in the next phase of history.

This is clearly going to be the case with the impact of the COVID-19.

I discussed this dynamic with my colleague Dr. Harald Malmgren who has focused for several years on a number of key emergent trends which in his view would now become dominant forces in the post-COVID-19 world.

Dr. Malmgren: We were seeing prior to the impact of COVID-19, a slow reconfiguration of where things are made, how they are made, and an underlying rethinking among manufacturers worldwide about the need to shorten supply lines.

We have been seeing significant changes in manufacturing technologies which allow for supply chains to be reconfigured in much closer proximity to manufacturing itself.

It is not about lowest labor cost; it is about having the most effective manufacturing cycle which includes security of supply as well.

This was not revolving around the China question but had already started several years ago with regard to manufacturing trends.

It became China-oriented in the last couple of years under Trump, but there was already in motion long-range planning for rearranging where things are made, and this process was not just occurring in the United States.

At the same time, politically, throughout the world, individual countries, and within those countries and within those nationals’ governments, we are having a reawakening of how to respond to threats to daily life at the local level, regional level, national level.

It’s particularly evident in the US, which is rediscovering that it’s a federation, not really a union in the true sense.

But because same process is being rediscovered as well within the European Union.

Improvisation is occurring in many forms.

In Europe of course we have very different responses in the visions throughout the countries through everything taking place and of course in Western Europe.

And then we have, huge differentiation between Spain, Italy, France in what they want to do collectively and what the Germans don’t want to do. Those lines of demarcation are hardening.

We are seeing clustering of responses, such as in Northern Europe on how to protect their interests, and how to defend themselves.

And with variable improvisation and clusterization of those responses, this will combine as a trend with the question of how manufacturing is recrafted and how trusted supply chains will be crafted.

It is a form of disaggregation of globalization but not about rejecting the notion of collaboration, but one not simply driven by the lowest labor cost at the end of a supply chain.

Question: And is it not likely that with the portability of capital, money will flow to those clusters capable of innovation and able to do so coming out of the gate more rapidly with regard to a post COVID-19 world?

Dr. Malmgren: It is highly unlikely that there will be an even spread of recovery worldwide. We will see significant migration, not just of people but of capital.

Within the United States, certain states will drive economic growth, at the expense of others.

Even though the United States is a Federal Government, the competition among the states will intensify as how states have managed the COVID-19 challenge will lead those states which had more realistic economic growth policies benefiting.

High tax states which have ignored economic growth requirements will see migration of people and capital which will drive differentiation and clusterization within the United States.

California versus Texas would be an example of where one might expect to see accelerated differentiation with regard to growth and development.

And we shall see the same trend in Europe. Investors are not nationally oriented; they are preservation of capital oriented.

They will be looking to invest in the emerging engines of growth for the next two years and they will move capital to areas where clusters of growth and innovation can be found.

And within Europe, again the gaps among nations in terms of creating favorable conditions for growth which were already significant prior to the crisis will grow.

This is historically similar to earlier periods of change such as the original industrial revolution.

For example, in the UK we are seeing a rebirth of the Midlands as engines of innovation in the digital domain, including artificial intelligence.

The response to COVID-19 and its aftermath will see a major reconfiguration taking place. The architects of the change are not going to be found in the Financial Ministries of France or Germany.

They will be driven by centers of innovation with the flow of capital to those centers, in which favorable growth strategies are prevalent.

The problem with the response to COVID-19 is that it has unleashed a number of governments in the states in the United States or in Europe that want to manage going forward with a state and tax dominated approach.

Those states in the United States or in Europe will find themselves severly disadvantage by the rapid growth of the new manufacturing revolution which encompass a new approach to managing supply chains as part of the reset.

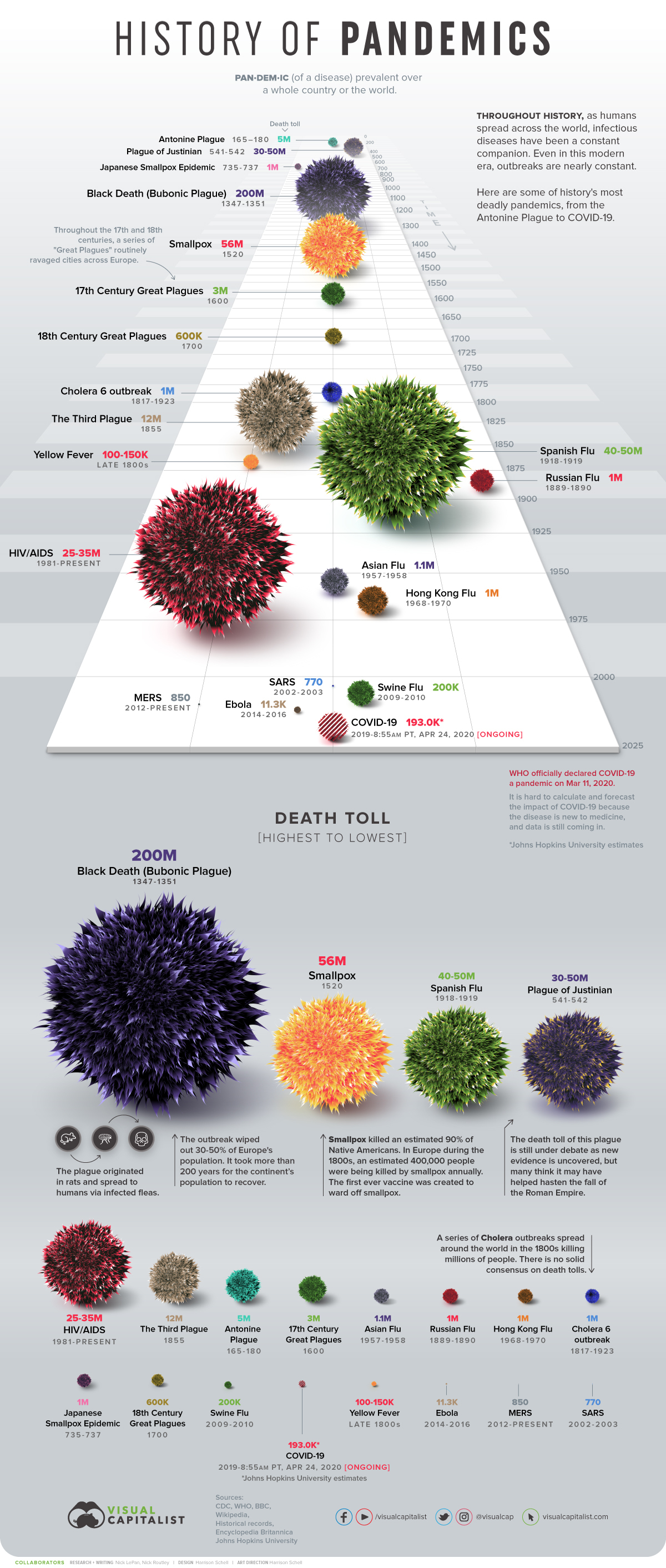

The featured graphic is credited to the following source:

history-of-pandemics-deadliest